All Categories

Featured

Table of Contents

Term plans are likewise commonly level-premium, yet the overage amount will continue to be the same and not grow. The most typical terms are 10, 15, 20, and three decades, based upon the demands of the insurance holder. Level-premium insurance policy is a kind of life insurance coverage in which premiums remain the very same price throughout the term, while the amount of protection provided increases.

For a term plan, this implies for the size of the term (e.g. 20 or three decades); and for an irreversible plan, until the insured dies. Level-premium policies will commonly set you back even more up-front than annually-renewing life insurance policy policies with terms of just one year each time. But over the long term, level-premium settlements are frequently a lot more economical.

They each look for a 30-year term with $1 million in insurance coverage. Jen buys an ensured level-premium policy at around $42 monthly, with a 30-year perspective, for an overall of $500 per year. Beth figures she might just require a strategy for three-to-five years or up until full repayment of her current debts.

So in year 1, she pays $240 per year, 1 and around $500 by year five. In years two with 5, Jen remains to pay $500 monthly, and Beth has actually paid a standard of just $357 per year for the same $1 million of insurance coverage. If Beth no much longer requires life insurance policy at year five, she will certainly have conserved a great deal of cash family member to what Jen paid.

What is What Is A Level Term Life Insurance Policy? Key Points to Consider?

Annually as Beth ages, she encounters ever-higher yearly premiums. On the other hand, Jen will certainly proceed to pay $500 each year. Life insurance providers have the ability to provide level-premium plans by basically "over-charging" for the earlier years of the policy, accumulating even more than what is required actuarially to cover the danger of the insured passing away throughout that early period.

Long-term life insurance coverage develops cash worth that can be obtained. Plan loans accrue rate of interest and unsettled policy fundings and interest will certainly reduce the survivor benefit and money worth of the plan. The amount of cash value readily available will usually depend on the kind of permanent plan acquired, the quantity of coverage bought, the length of time the plan has actually been in pressure and any type of outstanding policy financings.

A complete statement of insurance coverage is discovered only in the plan. Insurance policies and/or associated bikers and attributes might not be readily available in all states, and plan terms and conditions might vary by state.

Level term life insurance coverage is the most simple method to obtain life cover. In this article, we'll clarify what it is, how it works and why degree term might be best for you.

What is a Term Life Insurance For Couples Policy?

Term life insurance policy is a kind of policy that lasts a particular length of time, called the term. You pick the size of the plan term when you initially take out your life insurance coverage.

Choose your term and your amount of cover. Select the plan that's right for you., you know your costs will stay the exact same throughout the term of the policy.

Life insurance covers most circumstances of fatality, however there will certainly be some exemptions in the terms of the plan.

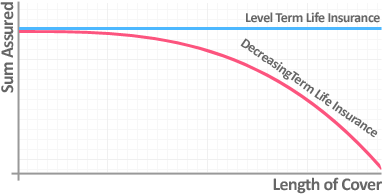

After this, the policy ends and the making it through companion is no more covered. Individuals usually obtain joint policies if they have impressive economic dedications like a home loan, or if they have youngsters. Joint policies are usually a lot more inexpensive than single life insurance policy plans. Other sorts of term life insurance plan are:Decreasing term life insurance policy - The quantity of cover reduces over the size of the plan.

Is Term Life Insurance With Level Premiums the Right Fit for You?

This safeguards the buying power of your cover quantity versus inflationLife cover is a great thing to have since it gives economic protection for your dependents if the worst occurs and you die. Your enjoyed ones can also use your life insurance payment to pay for your funeral. Whatever they pick to do, it's terrific assurance for you.

Nonetheless, degree term cover is terrific for meeting everyday living expenses such as family expenses. You can also use your life insurance policy advantage to cover your interest-only home mortgage, repayment home loan, school fees or any type of other debts or ongoing settlements. On the other hand, there are some downsides to level cover, contrasted to various other kinds of life policy.

Term life insurance policy is an economical and simple choice for lots of people. You pay premiums every month and the protection lasts for the term size, which can be 10, 15, 20, 25 or 30 years. Level term life insurance definition. Yet what happens to your premium as you age depends upon the kind of term life insurance policy coverage you acquire.

What is Increasing Term Life Insurance? A Simple Breakdown

As long as you continue to pay your insurance costs every month, you'll pay the very same price throughout the whole term length which, for lots of term plans, is typically 10, 15, 20, 25 or thirty years. When the term ends, you can either choose to end your life insurance policy protection or renew your life insurance policy, typically at a greater rate.

As an example, a 35-year-old woman in exceptional health and wellness can get a 30-year, $500,000 Place Term plan, issued by MassMutual beginning at $29.15 per month. Over the following thirty years, while the plan is in location, the price of the protection will not alter over the term period - Direct term life insurance meaning. Let's face it, most of us don't like for our expenses to expand in time

Your level term price is identified by a variety of aspects, many of which are associated with your age and wellness. Other aspects include your specific term plan, insurance coverage service provider, advantage quantity or payment. During the life insurance coverage application procedure, you'll respond to concerns regarding your health background, including any kind of pre-existing problems like a critical health problem.

{kind=link}

Latest Posts

Instant Insurance Life Smoker

Selling Final Expense Insurance Over The Phone

Best Funeral Insurance Companies