All Categories

Featured

Table of Contents

Degree term life insurance policy is among the most inexpensive insurance coverage choices on the market due to the fact that it offers basic protection in the form of death advantage and just lasts for a collection amount of time. At the end of the term, it expires. Entire life insurance policy, on the other hand, is dramatically more pricey than degree term life since it does not end and features a cash value feature.

Rates may vary by insurance firm, term, protection amount, health course, and state. Not all policies are readily available in all states. Price picture valid as of 10/01/2024. Degree term is an excellent life insurance alternative for many people, however relying on your coverage demands and personal circumstance, it may not be the very best suitable for you.

What types of Level Term Life Insurance Quotes are available?

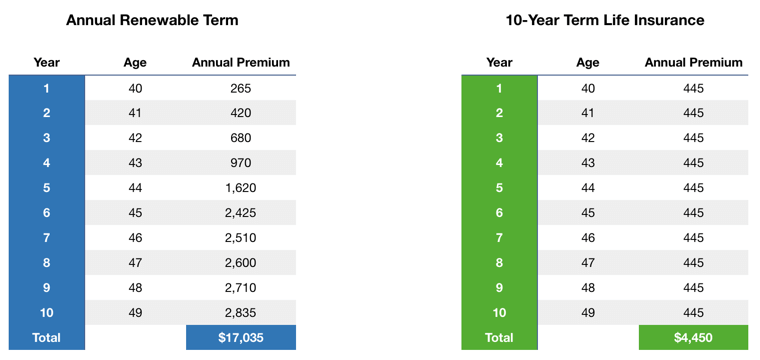

Annual renewable term life insurance policy has a term of just one year and can be restored each year. Yearly eco-friendly term life premiums are at first lower than degree term life costs, but prices rise each time you restore. This can be a great alternative if you, as an example, have just stop smoking and need to wait two or three years to request a degree term plan and be eligible for a lower price.

With a lowering term life policy, your survivor benefit payment will reduce gradually, but your repayments will remain the exact same. Decreasing term life policies like mortgage security insurance normally pay to your lender, so if you're looking for a policy that will certainly pay out to your loved ones, this is not a great fit for you.

Boosting term life insurance plans can aid you hedge versus rising cost of living or strategy monetarily for future children. On the various other hand, you'll pay even more ahead of time for much less coverage with a boosting term life plan than with a level term life plan. If you're not sure which kind of plan is best for you, collaborating with an independent broker can help.

Why should I have Level Term Life Insurance Rates?

When you have actually determined that degree term is best for you, the following step is to buy your policy. Here's how to do it. Calculate just how much life insurance policy you need Your coverage quantity ought to attend to your family's long-term financial demands, including the loss of your income in case of your fatality, as well as debts and day-to-day expenditures.

As you search for methods to safeguard your monetary future, you've likely discovered a variety of life insurance choices. Choosing the right coverage is a big decision. You wish to discover something that will certainly help support your liked ones or the causes vital to you if something happens to you.

Lots of people lean towards term life insurance policy for its simpleness and cost-effectiveness. Term insurance policy contracts are for a fairly short, defined duration of time however have choices you can tailor to your demands. Particular advantage choices can make your premiums change with time. Degree term insurance policy, nevertheless, is a sort of term life insurance that has regular payments and a changeless.

Is there a budget-friendly Fixed Rate Term Life Insurance option?

Level term life insurance is a subset of It's called "level" since your costs and the advantage to be paid to your loved ones continue to be the exact same throughout the agreement. You will not see any kind of adjustments in cost or be left questioning its value. Some contracts, such as yearly sustainable term, might be structured with costs that boost gradually as the insured ages.

They're identified at the start and remain the same. Having constant payments can aid you much better strategy and budget because they'll never ever alter. Level term life insurance. Repaired survivor benefit. This is additionally evaluated the start, so you can know specifically what death benefit amount your can expect when you die, as long as you're covered and updated on premiums.

No Medical Exam Level Term Life Insurance

This commonly between 10 and three decades. You accept a set premium and fatality advantage for the period of the term. If you die while covered, your fatality benefit will be paid to loved ones (as long as your premiums are up to day). Your recipients will certainly know beforehand how a lot they'll get, which can assist for intending purposes and bring them some financial safety.

You might have the choice to for one more term or, most likely, restore it year to year. If your contract has an assured renewability stipulation, you may not require to have a new clinical exam to maintain your insurance coverage going. However, your premiums are most likely to boost because they'll be based upon your age at renewal time. Level premium term life insurance.

With this option, you can that will certainly last the remainder of your life. In this case, once more, you may not need to have any brand-new medical exams, yet premiums likely will rise because of your age and brand-new protection. Various business provide various choices for conversion, make sure to understand your selections prior to taking this step.

Most term life insurance coverage is level term for the period of the contract duration, yet not all. With lowering term life insurance coverage, your fatality advantage goes down over time (this kind is usually taken out to particularly cover a long-term debt you're paying off).

Why should I have Level Term Life Insurance For Families?

And if you're established for renewable term life, after that your premium likely will rise yearly. If you're checking out term life insurance policy and wish to make sure simple and predictable monetary security for your family, level term may be something to take into consideration. Nevertheless, as with any kind of kind of insurance coverage, it may have some limitations that do not satisfy your requirements.

Commonly, term life insurance policy is more affordable than irreversible coverage, so it's a cost-effective method to protect financial security. Flexibility. At the end of your contract's term, you have numerous alternatives to proceed or carry on from coverage, typically without needing a medical test. If your budget plan or insurance coverage requires change, survivor benefit can be decreased in time and lead to a lower costs.

Can I get Guaranteed Level Term Life Insurance online?

As with various other kinds of term life insurance, once the contract finishes, you'll likely pay greater premiums for protection due to the fact that it will recalculate at your current age and health. Level term supplies predictability.

However that does not indicate it's a fit for everyone. As you're shopping for life insurance, here are a few key variables to consider: Spending plan. Among the benefits of degree term insurance coverage is you know the expense and the survivor benefit upfront, making it easier to without stressing over boosts over time.

Typically, with life insurance coverage, the healthier and more youthful you are, the much more budget friendly the insurance coverage. Your dependents and financial obligation play a duty in establishing your insurance coverage. If you have a young family, for instance, degree term can aid give economic support throughout important years without paying for insurance coverage much longer than necessary.

{kind=link}

Latest Posts

Instant Insurance Life Smoker

Selling Final Expense Insurance Over The Phone

Best Funeral Insurance Companies